It’s fair to say that the dust has far from

settled on the ramifications of the Hayne Royal Commission. With potential

civil and criminal charges to come and sweeping changes recommended to mortgage

broking, superannuation and the regulatory bodies, amongst others, there’s

plenty of fight left in this dog.

However, the consensus seems to be that many of

the sectors that picked up the biggest headlines got away relatively scot-free

in terms of outcomes. For example, there was no demand for the banks and their

wealth management arms to be forcibly separated, even though this is a move

that most of the the Big 4 pre-empted by looking to divest their wealth

business units (even if NAB may be walking this back).

There is a general perception that thanks to the

Commission, trust in the Big 4 (plus AMP) is shattered, which, if true should

have significant ramifications to at least the short-term prospects of these

major players.

However, the release of the commission’s report

saw a $19bn rise in the Big 4’s value as investors jumped on the outcomes and

as we all know, the markets generally don’t lie.

So we asked ourselves, ‘trust and banking makes a

great headline, but does it reflect the reality?’

Is trust

shattered or not?

The story in the media is that trust in the major

institutions is at rock-bottom, while the team at Yell has a more nuanced view.

Yell’s own research into trust

and financial services, has shown a general downwards trend of

consumer trust in the industry and specifically the banking category.

Admittedly, it’s coming off a relatively low base, however, we’ve yet to see

trust plummet off a cliff as the headlines suggests.

In the meantime, according to recent Roy Morgan

research, customer satisfaction, while on a slight

downward trend, still remains high.

This got us thinking. When we ask consumers if

they trust their bank, what does that actually mean? Trust them to do what?

What does

trust mean in an experience-based society?

We’ve long contended that trust in financial

services is inextricably linked to the core experience delivered day-to-day.

For most people, their experience is exceptional. Digital interactions have

changed our lives for the better, giving us better visibility and control of

our money. Therefore, the perception is that for most people, banks can be

trusted to deliver the day-to-day experience.

As we approached the tail-end of the Commission,

we knew that this theory was being tested, and it was time to do a deeper dive

into the motivations behind consumer trust in financial services. We broadened

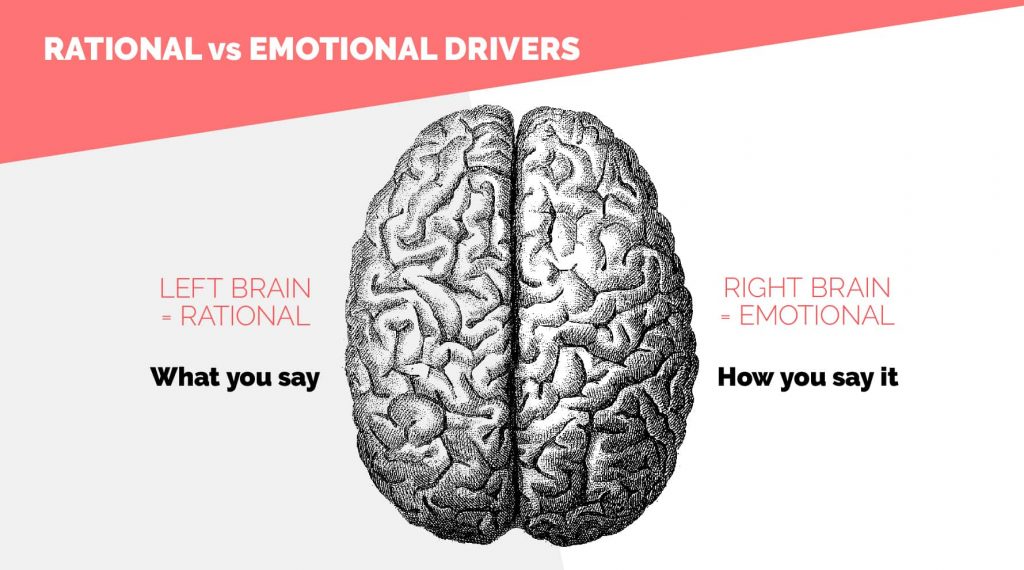

out the questions to include both rational and emotive responses, essentially

splitting out asking about what financial firms do, from how they do it.

Partnering with research firm Ipsos, we asked

consumers about their perceptions of a number of industry sectors including

banking, super, insurance and wealth management. The results uncovered insights that further

reinforced our belief that in an experience-centric society, delivering an

exceptional interaction experience can cover up a multitude of sins.

However, when it comes to perceptions of putting

the customer first, in many cases, especially the Big 4 banks, trust falls

through the floor.

Rational

vs emotional drivers and their influence on trust

The impact of delivering on a functional

experience cannot be underestimated. This may be why in part the markets rose,

why bank profits still continue to break records and why AMP has seen the main

impact of the Commission’s findings.

It’s also why significant investment continues to

pour into incremental improvements in the (primarily) digital experience of the

Big 4 banks.

It raises the question – If your bank does what

is says it’s going to do, gives you access to your money, keeps it safe and has

technology that allows you to perform your primary financial tasks – does it

matter how it acts? Given the recent financial and market performance, the

answer appears to be no, but that may be changing.

AMP on the other hand, doesn’t have that same

role in people’s everyday lives. Primarily having a focus on wealth and super,

both long-term and relatively low-touch experiences, it’s harder for it to

deliver an experience of functional outcomes that make a difference on a day to

day basis.

There’s clearly a multitude of other strategic

issues that AMP is having to contend with, but without that ability to

demonstrate a functional utility like the big banks, it’s possible that it

lacks the foundation of functional trust on which to depend and rebuild its

connection with its customers.

The

impending rise of emotional connectivity and trust

While functional utility delivers on the core

foundations of trust, we believe the opportunity lies in delivering on the

emotional drivers too. This is where our research shows that the Big 4 are

perceived to fall over and may be

where new and existing providers can deliver an

appealing alternative.

Once again, our research suggested that while

approximately a third of Australians are happy with their existing financial

services providers, there is a significant number who are open to considering

that change, or are actively considering changing providers.

There is likely a difference between the stated

intent of those we researched and the action they will take, especially given

the arduous nature of changing your whole of banking relationship. However, it

does appear that consumers will be more open to greater consideration of other

providers when they have a new banking need.

While this may not mean that the consequences of

distrust of the Big 4 will be a collapse of their ‘whole of wallet’ customer

base, it will likely see an erosion of parts of their offer to new and existing

entrants which present a more appealing customer story.

The opportunity is for those organisations not

caught in the full glare of the Royal Commission to offer credible alternatives

when the time is right. That means delivering on functional outcomes comparably

to their existing providers, while seeking to meet the emotive needs that

differentiate themselves from the Big 4 (and AMP).

Want to

find out more?

The Yell team is spending March offering to

present the latest insights on trust and the Royal Commission from our Ipsos

research and we’d be happy to share the outcomes with you and your team.

If you’d like to have us present to you and your team, please contact me at nigel@yellcreative.com